Recently, all media reported of how a social media apps CEO was grilled in the Hill. From the Q&A, one cannot see data that support the claims that the apps does or does not affect the users. Reported recently that the apps has negative impacts, especially among the younger generation. Click here for reading the report. However, the story was quoted from just one-person. As a Data Scientist, one needs not to make any decision or conclusion only based on limited observation for it is practically impossible to justify and make strategic decisions because of one observation. In order to find better answers on the issue, AAEA is conducting a survey, and we invite everyone all over the world to participate by clicking the following link:

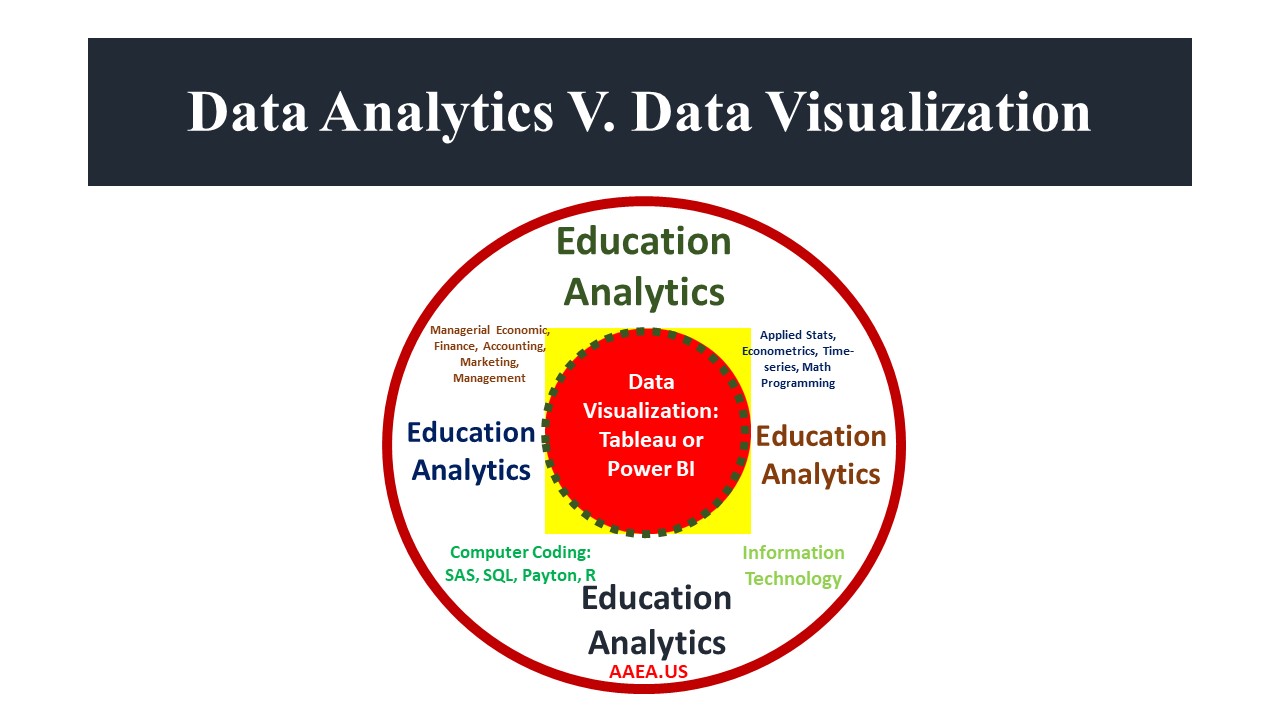

The IRI or EA (Education Analytics) is a great approach to study all aspects of Colleges’ operations–not just teaching or learning outcomes, but also institutional financial aspects. Never been shared before, how financial strengths can be measured by IRI/EA, but in this site. Exactly ten yeas ago (March 23, 2013), the Association has completed and shared these studies to test the US higher education institutions’ financial strengths which is equivalent to the required stress tests on the Banking industry after 2018 financial crisis hit the country. To accomplish such research tasks, AAEA first pulled the college financial information along with other data found at NCES database that covered 2008 through 2010. The data set consist of 16729 observations and 63 variables or fields–which after cleaning generate the following results (please click here to access the results). This example, one again demonstrates why higher education institutions in the US is better-off to have someone who is well rounded and capable to carry out the analyses. An expert that has various business and economic knowledge along with solid statistical analyses and econometric modeling experience will help the institutions to study their historical internal data which can be utilized in making strategic decisions. Data visualization is helpful, but no longer enough in today’s world marked with hyper-competition to attract the best brains in the world (not just in the US), as well as donation dollars.

Data Science (DS) profession has developed faster than EA. The adoptions of DS by all industry types have begun many years ago, especially by the credit card companies. After the Association was established, DS adoption has accelerated in the fastest pace in part because of the technology advancements, market competition, availability of big data gathered through internet, and the availability of cheaper data storages.

Majority of higher education institutions in the US are offering Data Science program at all levels, i.e., Certificates, Undergraduate, Masters’ and Ph.D.

However, the EA adoption, by US Colleges and Universities is lagging. Compared to the non-education industry. That is to say, the growth of EA adoption is not significant enough. The question that one might have is, why?

Harvard University took the lead to encourage higher education institutions in the US to apply or use institutional historical data in decision making process. Traditionally, this role supposed to be promoted through Institutional Research Association. However, past data showed that most institutions stressed two areas (1). Reporting purposes to both federal, state entities such as IPEDS as well as private data gathering organizations such as USNEWS or College Board; and (2). The most that Colleges and Universities did in the past were to have some sort of data visualization, generated mainly using Excel, before adopting either Tableau or Power BI software.

The College of Education at Harvard, through the Center of Education Policy Research launched the so-called the Strategic Data Project (SDP) initiative. Various programs are offered under the SDP project, where recently not only higher education institutions can participate in the initiative, but also PreK-12 institutions well. Harvard has taken the lead to promote data-driven decision making process for higher ed, for it has the abundant resources to accomplish such important roles.

The move that the Center has made shown that the era of making strategic decisions based on institutional historical as well as regional, state and national data has arrived, and left BAU as a history. It is truly an exciting development. However, the work has just begun, and much more need to be done. Exciting future opportunities are awaiting to be grasped.

No one knows, if this event will actually happen in reality. However, if it does, then the blue isle will have a huge boost. Even though, the event may occur years away, the results can be predicted today. The 2022 recent midterm election results are the future projection of 2024 big-dance, especially if the red color support this matchup. Strong data on current economics performance, low unemployment rate, and more importantly strong supports from the younger generation voters who have seen how the blue has helped making their life quality better, through, for example, the student loans forgiveness policy, and widely-opened employment opportunities. Therefore, there will be no surprise, if the 2020 matchup results would repeat the 2022 midterm election results. Go, and vote!

Disclaimer: This BLOG article does not suggest any readers to take any trade positions in the market; nor will it suggest taking trade strategies, or buy-and-sell any particular stocks.

One thing for sure–with the midterm election results were known, not only that it eases some level of uncertainties, but also the effects may have been capitalized last week The market, based on past data, showed that as the uncertainties were pressed down, the DOW will react in green. However, Market may concern more about inflation than the midterm results. In addition to that, there are elephants which may affect the magnitude of market reactions–which may drag the NASDAG in the red zone. Another note, the DOW gained more than 1000 points on one trading day, last week, which usually follows by a red movement. How high (low) will it go green (red) this week, will depend on how the market will think collectively, and the assessment on the equity market–either it is undervalue (overvalued). Will find out soon.

Data tell the truth. It is now clear–the results of the midterm elections have revealed the American voters’ collective rationality and decisions. AAEA has written several articles, and based on data to project what will happen with the voters choice–and it did. The results show that the American people have chosen democracy against an experiment to change the current formed of government to a totalitarian system experimented by thirst-for-power, and an ego-centric nuisance. The voters know that they are better-off for sure under a circumstance to pay a little higher price at the grocery stores, but still keep their job compared to a worse situation of getting fired by employers. Congrats America!!

Needless to say that corporations are pressured by the Wall Street to make positive ROI. Therefore, most, if not all US corporations have relocated their production to the third-world countries. Especially, in the Southeast Asia region. This outsourcing production, not only embraced by labor-intensive industry, such as shoes companies, but also by other industries. Starting in the 1980’s, and based on core-competency hypothesis, the US and corporations from developed countries justified their production relocation to the so-called cheap-labor countries. This strategy was seen very logical because the investors from the home countries have to finance the fixed assets related to manufacturing facilities such as machineries, land and above all have to deal with the home-country labor regulations. Often, this so-called join-venture are welcomed and enjoy the tax-holidays for years.

As the home countries developed their economy, and more economics opportunities were opened, more and more workers have alternative choices and start realizing their bargaining power. Therefore, after 40 years, labor are no longer cheap as it was in the past. As labor cost increases, not only that it causes higher production cost, but also lower the bottom line. Therefore, to meet the Wall Street’s expectation, corporations were forced to increase their selling price in the US market which finally causes inflationary condition to the economy. Folks needs to remember that they have enjoyed the cheap-price because the developing countries workers have absorbed those price increases in their own-hand. Without them, the US inflation could have happened many years ago. Forty years in the making is just awfully long period, where they–the workers from developing countries such as in the Philippines, Laos, Bangladesh, India, Vietnam or Indonesia and others have to shoulder price increases in the US consumers market.

On October 24, 2022 AAEA has shared its analyses, and predicted, based on logic, and data that the next choice of macro policy will finally lead towards keeping the employment instead of pressing further with hiking the interest rate at all cost. Our simple analyses using Econ 101 shows that, given what is happening in Europe, Americans will be much better-off to pay a little higher price at the grocery stores against losing their jobs. These analyses have been proved to calm down the WallStreet, help law makers to understand the issues, and shed the light to the Labor Secretary.

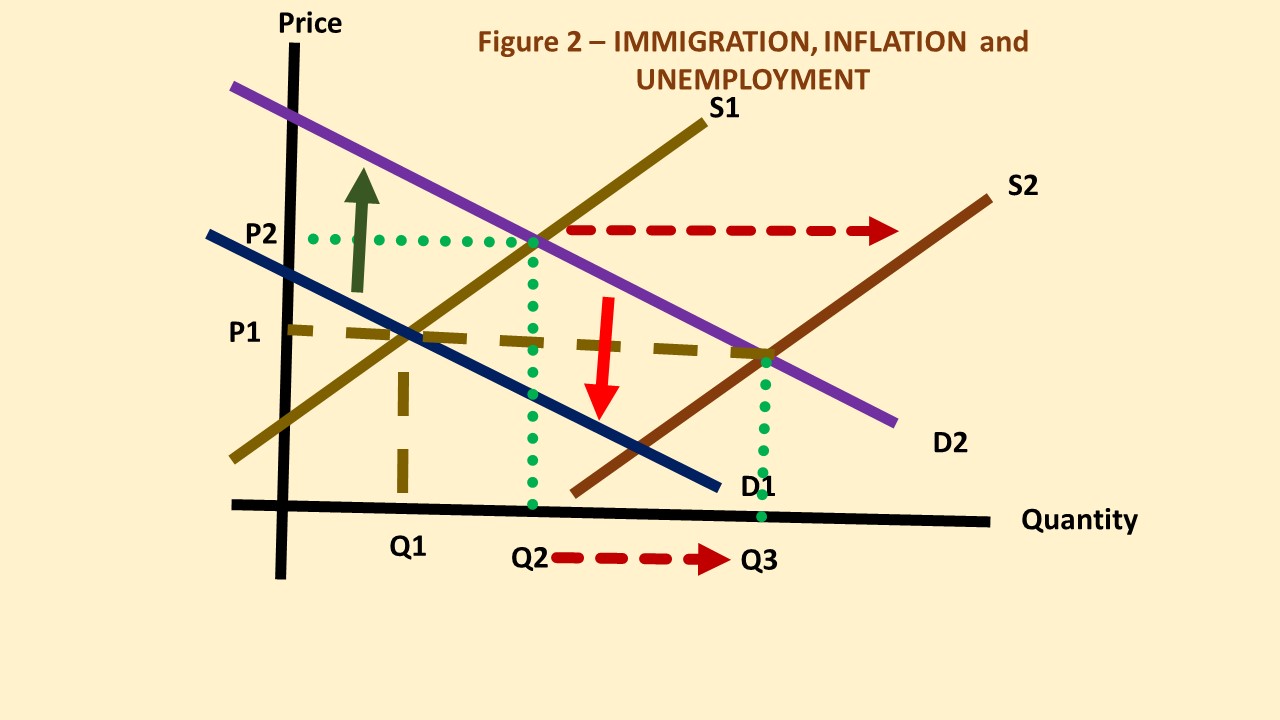

After we published the analyses, the DOW has consecutively move upwards for 4 days in a row. Another AAEA article written on October 26, post a question of why the US cannot produce more goods and services, which in-turn will be able to manage the inflationary situation, by increasing the aggregate supply from S1 to S2. This movement reflects by a gradual increase on national output from Q1 to Q3. A better-than expected growth on US GDP was reported on October 27, which in-turn have proved that the economic growth is moving toward the right direction. According to AAEA analyses, these movements have helped suppressing the inflationary pressures. With all these facts and analyses, the US consumers need to know that the economic policy from the current administration is working. Nothing will go a hundred percent perfect–but most Americans prefer to have their jobs, and will to pay a little higher grocery price, rather than being unemployed.

We have discussed the probable reasons why the negative impacts of labor shortages have gotten more problematic recently. In many years, the US corporations have relocated their production capacities to countries with low labor cost. As results, one can easily finds household stuff made in other countries, rather than the US. While this move is justifiable from the profit maximization according to the new-classical point of view– it is actually a delayed of inflation to occur in the US. The problem of inflation should have happened a decade ago or longer, but it got absorbed by other countries, for example in the Southeast Asia. The population in these countries are the real heroes who have shouldered the US consumers from paying higher prices. This past summer, AAEA did a simple on-the-ground survey of product origins. It was not a shocking to find, aside from the produce, more than 90 % stuff were sold at one of the national chains are made in China. Though, the economic analyses show that labor shortages are the culprits of why the US cannot increase its national product in a fastest rate, it is obvious that the industry sector has chosen a short-cut to achieve the Wall Street’s expectation by relocating their production outside the country. These strategies are fine in the short-run, but proved to be costly in the long-run, as it is shown now.

So, when the developing countries make progress in their economy, so do their bargaining power. They will ask more for their own labor, or there will be no output produced. As labor are more expensive overseas, then corporation simply passed those extra cost to their end-consumers in the US market.

Well, hopefully the two isles see the lights, and the reasons why inflation is skyrocketed, and why the border is broken. No need to bus people to NYC. Accommodate them to rise long-horn cattle, or to grow strawberries, or whatever that produce something counted to add into the GDP.

To solve higher inflation, while keeping unemployment in-check is explained in Figure-2 above.

Any policy maker could, in theory push the aggregate demand down toward D1 by shifting the supply curve from S1 to S2. By doing so, more goods and services can be produced–shifting the national output from Q2 to Q3. The question that one might ask is that, why can’t the US pursue this obvious path? Well, as one has learned, again from Econ 101, it all depends on the availability of factor of productions (resources), such as, among other factors, are labor, land, capital, technology, entrepreneurship, etc.

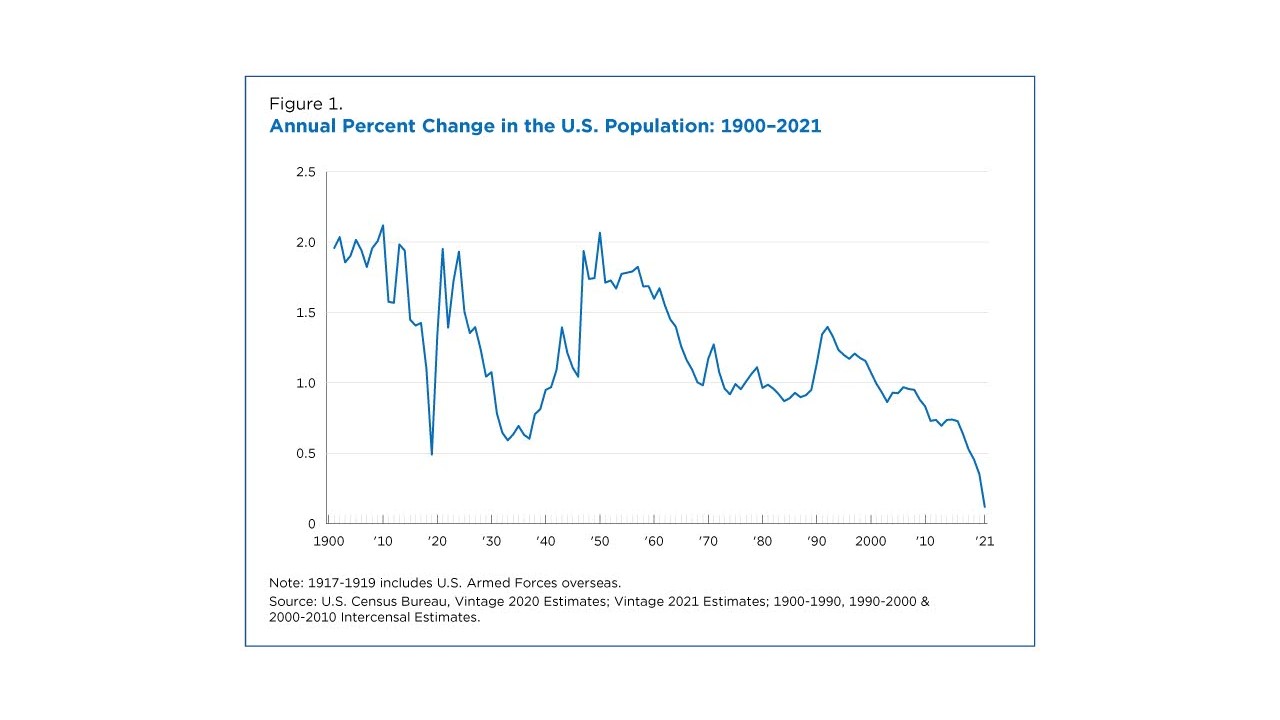

Since the current labor in the US is finite, it will take time, efforts and money to prepare workers up to a point that they are ready to participate. This labor shortages in no doubt affect the US ability to produce output at Q3 level. So, should Uncle Sam wait until the labor becomes available, or manage what is available currently? Based on recent publication from the US Census Bureau, it is pretty obvious that the country has experienced a steady population growth declining, which accelerated starting in 2020. The impacts of labor shortages are obvious, so does the price that the Americans have to pay at the grocery stores.

Perhaps, and AAEA hopes, that these analyses help both the opponents and proponents of immigration debate to understand these complex issues. The inflation-employment analyses need to be tied to the input market. If the public policy restricts the movement of labor that is coming to this country, surely S2 cannot be shifted fast enough to keep up with the growth in demand. As results, inflation is going up.

This graph is taken from the Census Bureau which shows that the US population annual growth has fallen steadily, even accelerated starting in 2020. The impacts are obvious.

The old saying exclaimed “it takes two to tango”. One cannot expect to pay a happy meal price for Osetra Caviar, at Atelier Crenn in San Francisco, California. Always remember–the cause and effect.